The dairy industry has spent the past few years navigating volatility, margin pressure, and structural change. While 2025 did not deliver a full-blown recovery, it did confirm something important: the cycle is turning, but unevenly.

Based on data from more than 140 dairy companies and global production and pricing signals, here are the key takeaways from our Dairy Industry Wrapped.

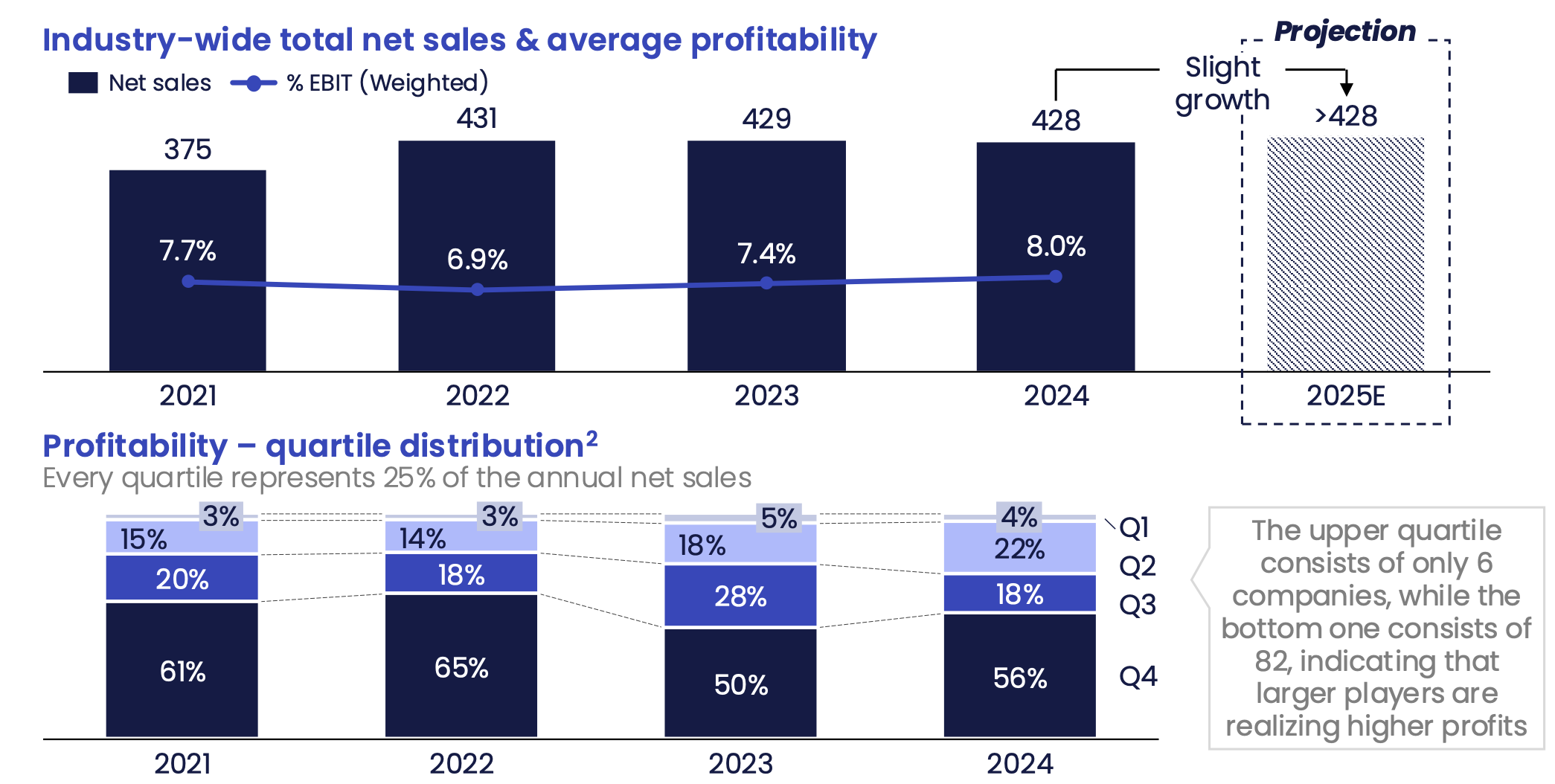

Learning #1: Profitability improved, even as sales stayed flat

Despite largely flat net sales over recent years, dairy companies managed to lift profitability in 2024. Average EBIT margins increased by roughly 0.6 percentage points, reflecting better cost control, portfolio focus, and scale effects among larger players.

Looking ahead to 2025, we expect slight net sales growth, supported by a strong first half of the year,

says Randy Steenbergen, senior market intelligence analyst at A-INSIGHTS.

However, profitability signals remain mixed. The gap between top and bottom performers is wide, with a small group of large players capturing a disproportionate share of industry profits, reinforcing a familiar conclusion: size still matters.

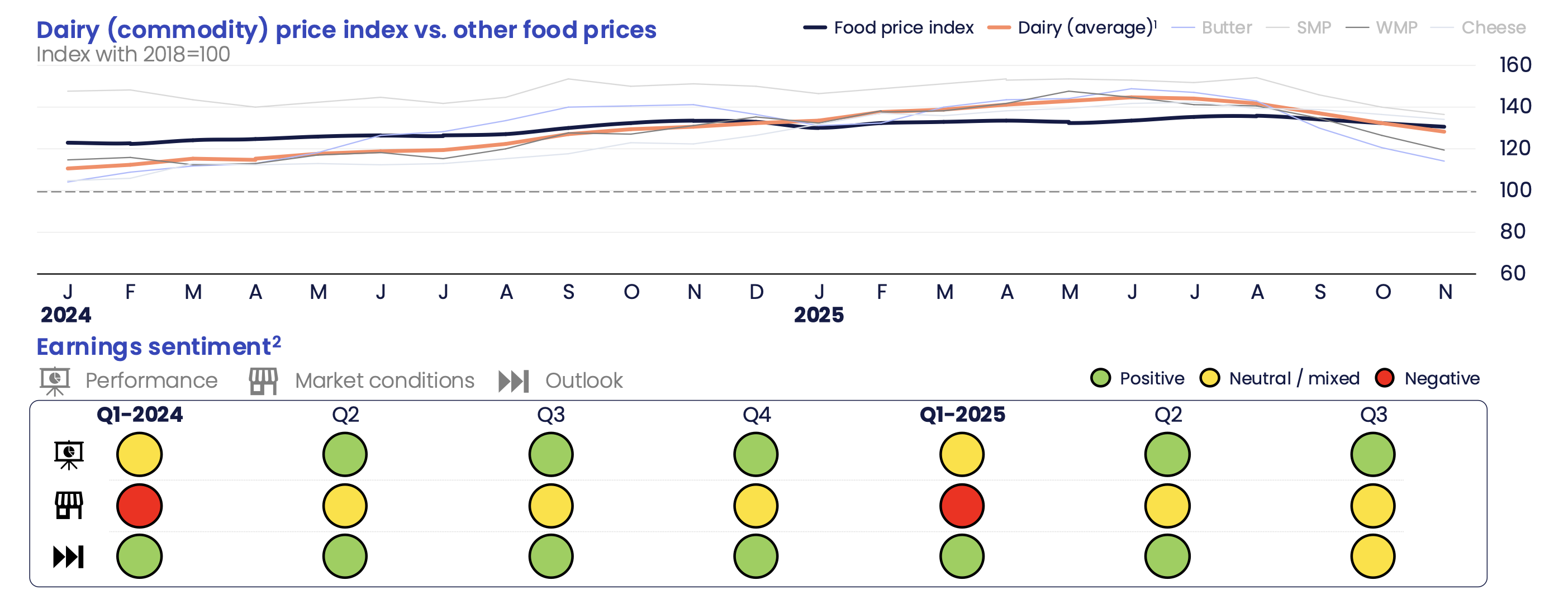

Learning #2: Dairy prices peaked mid-2025 and sentiment followed

Dairy commodity prices climbed steadily into mid-2025, outperforming broader food price indices. But the momentum did not last. Prices peaked halfway through the year and declined into Q3, triggering a visible shift in earnings sentiment across the industry.

What stood out was not just the price move itself, but the speed with which market confidence softened. While performance indicators remained relatively resilient, outlook sentiment turned more cautious: it's a reminder of how exposed the sector remains to commodity dynamics.

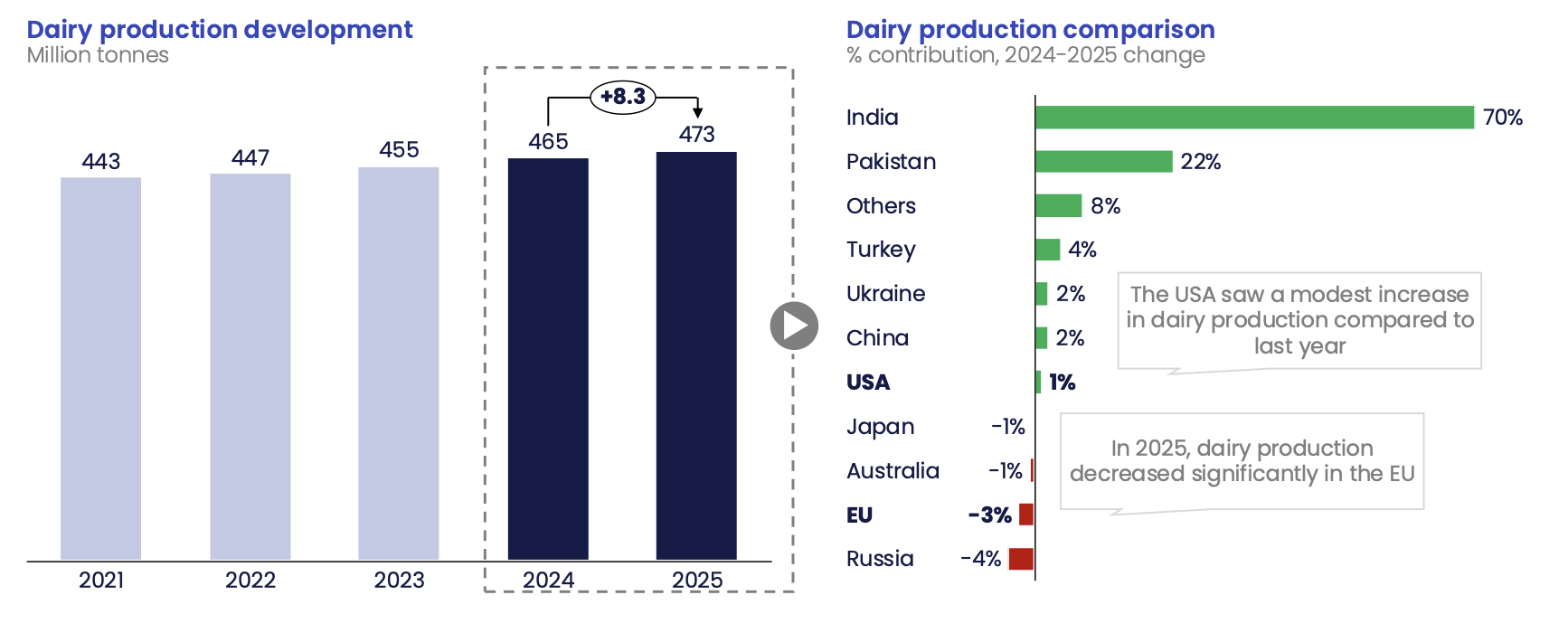

Learning #3: Global supply growth is real but uneven

On a global level, dairy production continues to grow. However, that growth is increasingly Asia-led and absorbed locally, particularly in India and Pakistan. Meanwhile, European milk supply is contracting, creating tighter regional balances and more volatility.

The US sits somewhere in between, with modest production growth and an opportunity to strengthen its role in global dairy trade as European supply peaks over the coming decade.

Learning #4: Strategy reset is well underway

Against this backdrop, dairy companies are actively reshaping their portfolios and strategies.

Recent announcements highlight a clear pattern:

- Large-scale mergers aimed at securing milk supply and resilience

- Divestments from consumer categories, particularly by CPG players

- Shifts toward B2B and ingredients

- Regulatory changes that may fundamentally alter pricing mechanisms in key markets

Together, these moves point to an industry preparing for a more volatile, uncertain, complex, and ambiguous (VUCA) environment and acting before the next downturn hits

What this means for 2026 and beyond

The dairy cycle is not “fixed,” but it is changing. Growth will be harder won, scale advantages will matter more, and regional supply dynamics will increasingly shape global trade flows.

For leadership teams, the challenge is clear: separate signal from noise, pressure-test assumptions, and align early on what really changed.

Never miss a beat on the dairy market

At A-INSIGHTS, we help dairy companies turn fragmented data into a shared fact base so leadership teams can make better, faster decisions as the cycle shifts.

Want to grab to receive next dairy updates in your mailbox? Subscribe to our newsletter.