Tracking the trends shaping the industry

Every month, we analyze the global frozen potato market to help you stay ahead in a fast-moving trade landscape. This edition highlights rising Middle Eastern imports and shifting European export dynamics, alongside intensifying competition from Asian suppliers.

Market pulse: trade stabilizes, but prices face continued downward pressure

In April 2025, global frozen potato trade volumes reached 812 thousand tonnes, marking a +1.3% year-over-year increase. Prices continued their downward trend, falling -3.7% to €1.28/kg.

For the year-to-date period (January–April 2025):

- Global trade volume rose by +1.4%, an increase of +45.0 thousand tonnes to 3,166 thousand tonnes.

- Average trade price declined by -3.0%, or €0.04/kg, reaching €1.29/kg.

Middle East imports increase driven by India, China, and Egypt–Europe loses share

Total frozen potato imports into the Middle East grew by +7.8% year-over-year in the first four months of 2025, adding +19.0 thousand tonnes to reach 263.8 thousand tonnes. This growth came amid falling average prices, which dropped €0.09/kg to €1.13/kg (-7.7%), creating opportunity for competitive exporters.

Intra-regional supply expands

Middle Eastern countries are increasingly sourcing from within the region, particularly from Egypt:

- Total regional exports to the Middle East grew by +39%, up +21.9 thousand tonnes to 55.6 thousand tonnes.

- Egypt was the primary driver, increasing exports by +19.1 thousand tonnes to 49.6 thousand tonnes (+62%).

- Jordan emerged as a major destination, importing 18.1 thousand tonnes, up from 7.6 thousand tonnes last year (+138%).

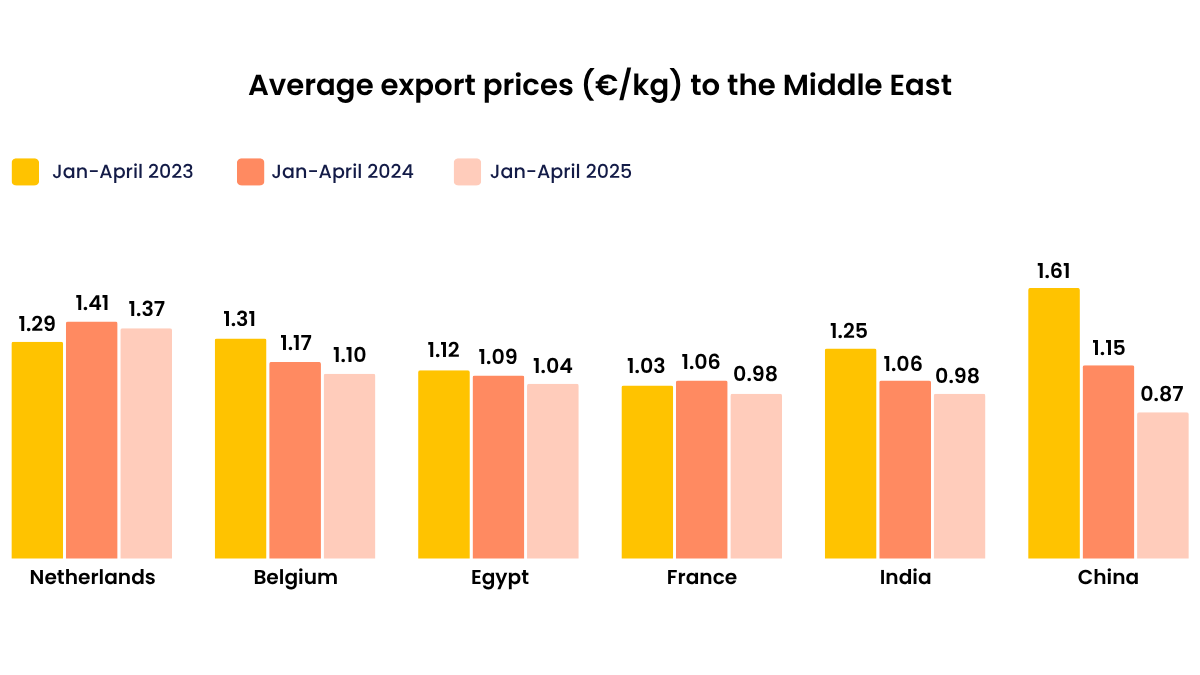

- Egypt’s average export price was €1.04/kg (-3.9%), more competitive than Belgium (€1.10/kg) but slightly above France (€0.98/kg).

This intra-regional trend highlights a growing preference for geographic proximity and price competitiveness in regional supply chains.

Asian exporters gain ground with price aggression

Asian exports to the Middle East surged by +424%, adding +25.7 thousand tonnes to reach 31.8 thousand tonnes year-to-date. The average price dropped €0.12/kg to €0.95/kg (-11.3%), reflecting highly aggressive pricing strategies.

- India exported 21.8 thousand tonnes, up from 5.8 thousand tonnes (+274%), at an average price of €0.98/kg (-€0.08/kg).

- China saw an exponential rise from 0.2 thousand tons to 9.9 thousand tonnes, with prices plunging €0.28/kg to €0.87/kg (-24%).

The sharp price drops suggest a strategic push by Asian exporters to penetrate and secure market share in the Middle East, especially in growing demand centers such as:

- Saudi Arabia: +12.0 thousand tonnes to 14.3 thousand tonnes (+537% YoY)

- United Arab Emirates: +6.6 thousand tonnes to 8.4 thousand tonnes (+382% YoY)

European exporters are losing ground

Despite being the region's main supplier, European exports to the Middle East fell by -18%, down -33.4 thousand tonnes to 154.8 thousand tonnes year-to-date. The average price dropped €0.07/kg to €1.19/kg (-5.2%).

- The Netherlands:

- Volume declined -7.3% or -5.0 thousand tonnes to 63.0 thousand tonnes.

- Export prices fell slightly to €1.37/kg (-€0.05/kg), remaining the highest among major suppliers.

- Belgium:

- Exports dropped sharply by -47.6%, or -46.1 thousand tonnes, reaching just 50.8 thousand tonnes.

- Prices declined by €0.07/kg to €1.10/kg.

- France:

- Increased exports by +98.4%, or +18.1 thousand tonnes, totaling 36.6 thousand tonnes.

- Prices decreased by €0.08/kg to €0.98/kg, on par with Indian prices.

The diverging performance between France and Belgium is likely linked to the recent opening of Clarebout’s Dunkerque facility. Still, the sharp volume losses - especially for Belgium - highlight the growing challenges European exporters face in competing with regional and Asian rivals on both price and responsiveness.

European crop outlook: European suppliers can benefit from strong harvest

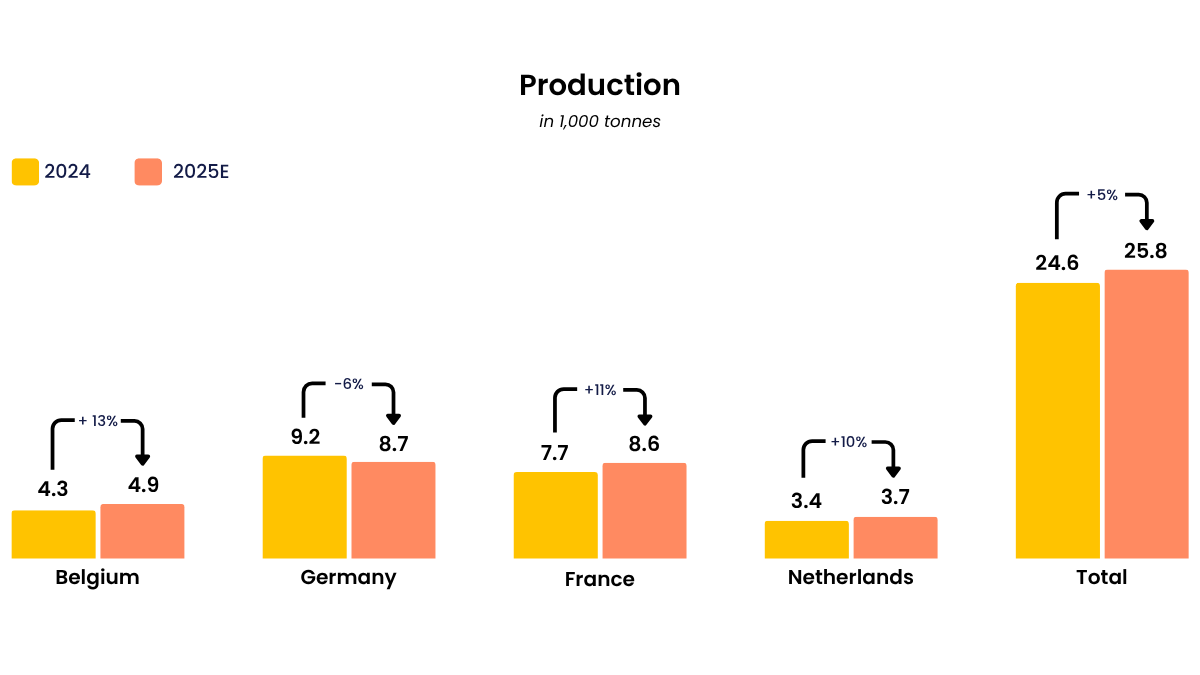

While competition from Asian and Middle Eastern exporters is growing, Europe’s production base is strengthening, offering a potential tailwind for European suppliers. According to the latest forecasts, the EU-4 potato crop (BE, DE, FR, NL) is expected to grow by +5% year-over-year, reaching 25.8 million tonnes. This growth is driven by both acreage expansions (+5% to 586 thousand hectares) and improved yields—with Belgium and the Netherlands seeing yield increases of +7% and +2%, respectively.

- Belgium: Acreage up by +6%, yields up +7%, and production rising +13% to 4.88 million tonnes.

- Netherlands: Acreage up by +9%, yields up +2%, and production up +10% to 3.73 million tonnes.

- France: A strong rebound in planted area (+10%) and stable yields are projected to lift production by +11% to 8.55 million tonnes.

- Germany: While acreage declines slightly and pests pressure crops in some regions, yields are only moderately impacted; production is expected to decrease by -6% to 8.65 million tonnes.

Crucially, the increase in raw potato volumes is likely to put further downward pressure on export prices, as raw materials represent the largest share of total production costs. This creates an opportunity for European exporters to regain market share, particularly in price-sensitive regions. With their highly efficient processing operations, European suppliers are well-positioned to strengthen their competitiveness on the global frozen potato trade market.

Why trade intelligence is more critical than ever

As global trade patterns shift, staying ahead requires more than intuition. With market access rules, tariffs, and competitive pricing strategies changing rapidly, processors, suppliers, and buyers need real-time, reliable insights to make informed strategic decisions.

At A-INSIGHTS, we deliver monthly updates based on official customs and statistical sources, providing the most accurate view of global frozen potato trade flows—covering volumes, prices, and supply shifts across regions.

Stay ahead of the curve

Want to understand how these developments impact your business?

Book a conversation with our team to explore how A-INSIGHTS can help you navigate market complexity and sharpen your strategic advantage.